Cleaves ” Long waiting times for VLGCs transiting the Panama Canal”

High traffic, seasonal fog and COVID-19 related issues had already led to congestion and long waiting times for VLGCs transiting the Panama Canal

High traffic, seasonal fog and COVID-19 related issues had already led to congestion and long waiting times for VLGCs transiting the Panama Canal, reports Norway’s Cleaves Securities. In an advisory note dated December 31, 2020, says Cleaves, “the Panama Canal Authority made transit even more challenging by disallowing VLGCs to book during Period 1.”

“Although Booking Period 1 is only applicable for dates starting three weeks ahead in time, and with plenty of slots open in Booking Period 2 (currently from January 8 to January 25), the change in policy seems more like a move to give regularly trading vessels with significant delay implications the ability to plan ahead,” says Cleaves. “Booking Period 1 is now reserved for “Neopanamax full container, passenger, and LNG vessels”.

That said, the first available slot in Booking Period 2 is January 13, nine days from now. The change in policy is obviously negative for LPG transportation (positive for VLGC spot rates) as it removes flexibility and adds further to the already existing fleet inefficiencies. We estimated a net 6.7% reduction in effective fleet capacity vs normal levels in our December 15 VLGC report.

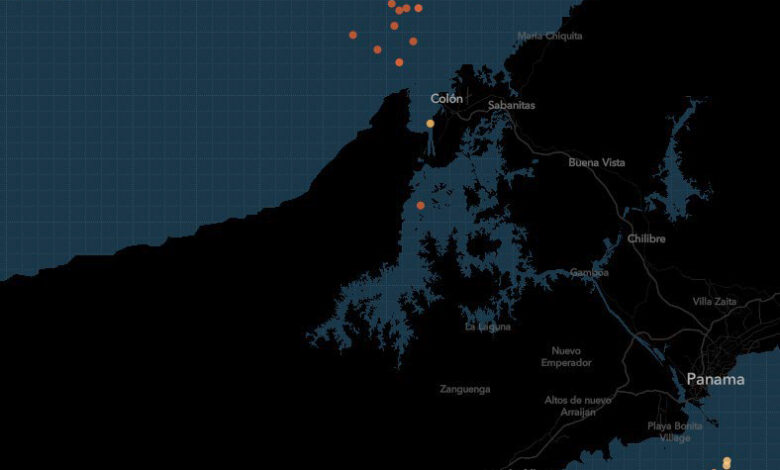

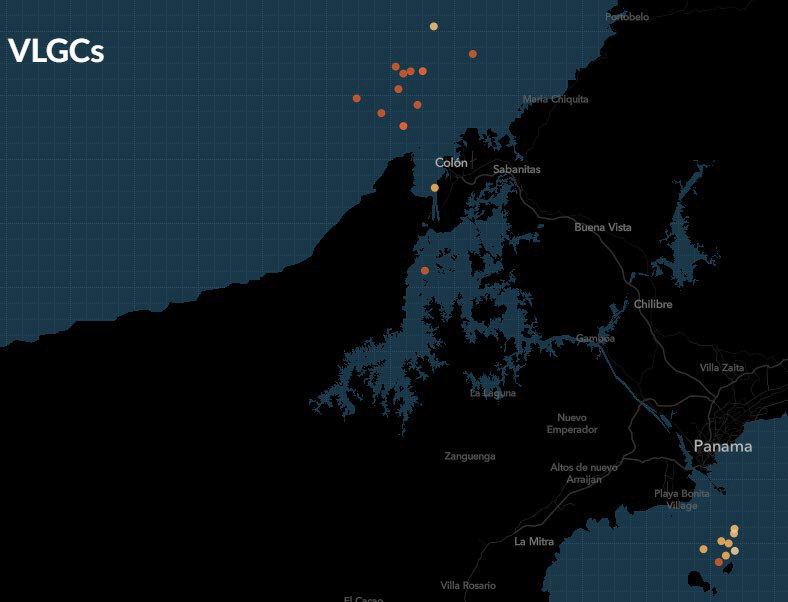

“Our satellite data shows that 17 VLGCs are currently awaiting Panama Canal transit, 10 laden vessels on the Caribbean side and 7 ballasters on the Pacific side. Additionally, there are 4 vessels under transit. This compares with the total of 14 vessels waiting on average in December and 5 in November. With some vessels now using more than 13 days to transit the canal (normally around two days), many opt for the ~12 days longer voyage around Cape of Good Hope, adding around 39% more time to the U.S/ Gulf to Far East voyage.

VLGC spot rates

“VLGC spot rates continues to show incredible strength, quoted at TCE $101k/d today. VLGC forward freight agreements (FFAs) surged today across the curve, potentially as LPG traders got nervous being caught short shipping in a red-hot market. The January FFA rose 5% to $115/t (vs spot at $109/t). The major gains were however further down the curve, with i.e. February +15% to $105/t, April +20% to $90/t and June +30% to an implied $82.5/t.

SELL ratings on the VLGC

“Our VLGC share price index has added 5% so far today (+70% since the lows in late October), likely due to the surging FFA-curve and the aforementioned news from Panama. Although our SELL ratings on the VLGC companies look unwise against a non-stop flow of positive news, we are still fearful that the near-term peak is close. We expect fleet inefficiencies to abate during 1Q21, which together with a potential 13% decline in US LPG exports q/q and falling Far Eastern LPG prices lead us to forecast VLGC spot rates significantly down by March. If our base case plays out, the risk to VLGC share prices is skewed towards the downside.”